A tenancy can look "done" the moment an offer is accepted — until affordability falls apart late in the process. That's when you lose time, lose landlord confidence, and often lose the tenant too. The fix isn't doing more checks. It's doing the right checks, in the right order, with a consistent decision framework that your team can apply quickly and fairly.

This guide gives you a practical, agency-ready affordability framework you can standardise across branches — to reduce fall-throughs, shorten time-to-move-in, and keep your risk decisions defensible.

Why landlords and agents care more than ever about affordability

Landlords increasingly judge agencies on certainty and speed:

- Certainty: fewer failed starts, fewer arrears risks, fewer awkward "we need more documents" loops.

- Speed: shorter void periods, faster tenant move-ins, less negotiation fatigue.

What is a tenant affordability check?

A tenant affordability check is a structured assessment of whether a tenant can sustainably meet rent payments (and associated living costs) for the duration of the tenancy — based on verified income, stability, and financial commitments.

It's not the same as a credit check, and it's not "gut feel". A good affordability check is:

- Evidence-led — documents and verification

- Consistent — same thresholds applied across cases

- Explainable — you can justify the outcome

- Proportionate — you only ask for what you need

Why affordability checks fail in practice

Most agencies aren't "bad at affordability" — they have problems with sequence and standardisation. Common failure modes:

- Checks happen too late (after holding deposits and admin has started)

- Thresholds aren't clear, so decisions vary by negotiator or branch

- Evidence is inconsistent (screenshots vs statements vs partial documents)

- Edge cases aren't handled (self-employed, contractors, overseas applicants)

- Guarantors are used reactively, not as a policy-led decision

The Affordability Framework

A 4-part model: simple, defensible, repeatable

- Income capacity — can they pay rent on paper?

- Income stability — is that income reliable?

- Commitment load — how much is already "spoken for"?

- Buffer / resilience — do they have margin for shocks?

This turns affordability from "opinion" into a decision record you can stand behind — useful for landlords, teams, and disputes.

Landlords don't just want a yes/no. They want a repeatable process that reduces nasty surprises after an offer is accepted.

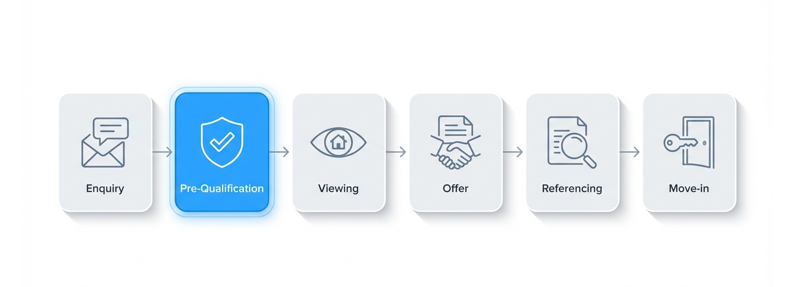

Step-by-step: the agency workflow

Set your policy — before the next applicant

You need a documented policy that states:

- Target affordability ratio (e.g., rent-to-income guideline)

- Minimum evidence by tenant type (employed, self-employed, contractor, overseas)

- When a guarantor is required

- What triggers a conditional pass vs fail

- Who signs off edge cases (e.g., branch manager / compliance)

This is what prevents disputes and inconsistent outcomes.

Collect minimum pre-qualification data — fast

Before you book viewings (or at least before accepting an offer), collect a lightweight pre-qual set:

- Monthly rent and move-in date

- Employment status and employer name

- Monthly take-home pay (or day rate / average drawings)

- Any other adult occupants contributing income

- Whether there's a guarantor available (if needed)

Goal: decide if the applicant is likely to pass affordability before you start deeper admin.

Apply a rent-to-income guideline — capacity check

A commonly used approach is a rent-to-income guideline (monthly or annual). You set the threshold once and apply it consistently. At minimum, calculate:

- Gross income multiple — annual income ÷ annual rent

- Net rent ratio — monthly rent ÷ monthly net income

- If the ratio is clearly healthy → proceed to verification

- If it's borderline → proceed as conditional pass pending stronger evidence or guarantor

- If it's clearly weak → stop early (save everyone time)

Verify income — evidence check

This is where agencies often lose time. Standardise the evidence list so your team doesn't improvise.

Employed (PAYE)

Ask for

- Last 3 months payslips

- Bank statements showing salary credits (matching payslips)

- Employment contract or employer confirmation (where needed)

Check

- Salary amount and regularity

- Probation period / start date

- Any major deductions that materially reduce take-home pay

Self-employed

Ask for

- SA302 / tax calculation + tax year overview

- Accountant letter (where available)

- 3–6 months business/personal bank statements

Check

- Profit consistency and seasonality

- Reliance on one client

- Evidence aligns with bank inflows (avoid "paper-only" income)

Contractors

Ask for

- Current contract + day rate

- Remaining contract duration + renewal likelihood

- Bank statements showing consistent income

Check

- Gaps between contracts

- Whether income is stable and likely to continue through tenancy

Overseas income / relocation

Ask for

- Offer letter / employment contract (UK role if relocating)

- Proof of funds and runway if moving before first payroll

- Bank statements from recognised institutions (translated where necessary)

Check

- Timing mismatch (move-in vs first income)

- Currency risk and transfer reliability (policy decision)

Assess commitment load — the "silent killer"

Two applicants can have the same income but very different affordability once commitments hit. What to look for:

- Regular high outbound payments (loans, childcare, maintenance)

- Multiple credit commitments

- High discretionary spend with low buffer

Keep this proportionate and consistent. The goal is not to "judge lifestyle" — it's to confirm there's room to pay rent reliably.

Apply buffers — resilience check

A resilient tenant can handle real life: a delayed payroll, a contract gap, an unexpected bill. Evidence of buffer can include:

- Savings (proof of funds)

- Stable employment tenure

- Low commitments

- Strong guarantor (pre-validated)

Buffers are particularly important for:

- High rent vs income cases

- Contractors and variable income

- Tenancies with multiple occupants and uneven contributions

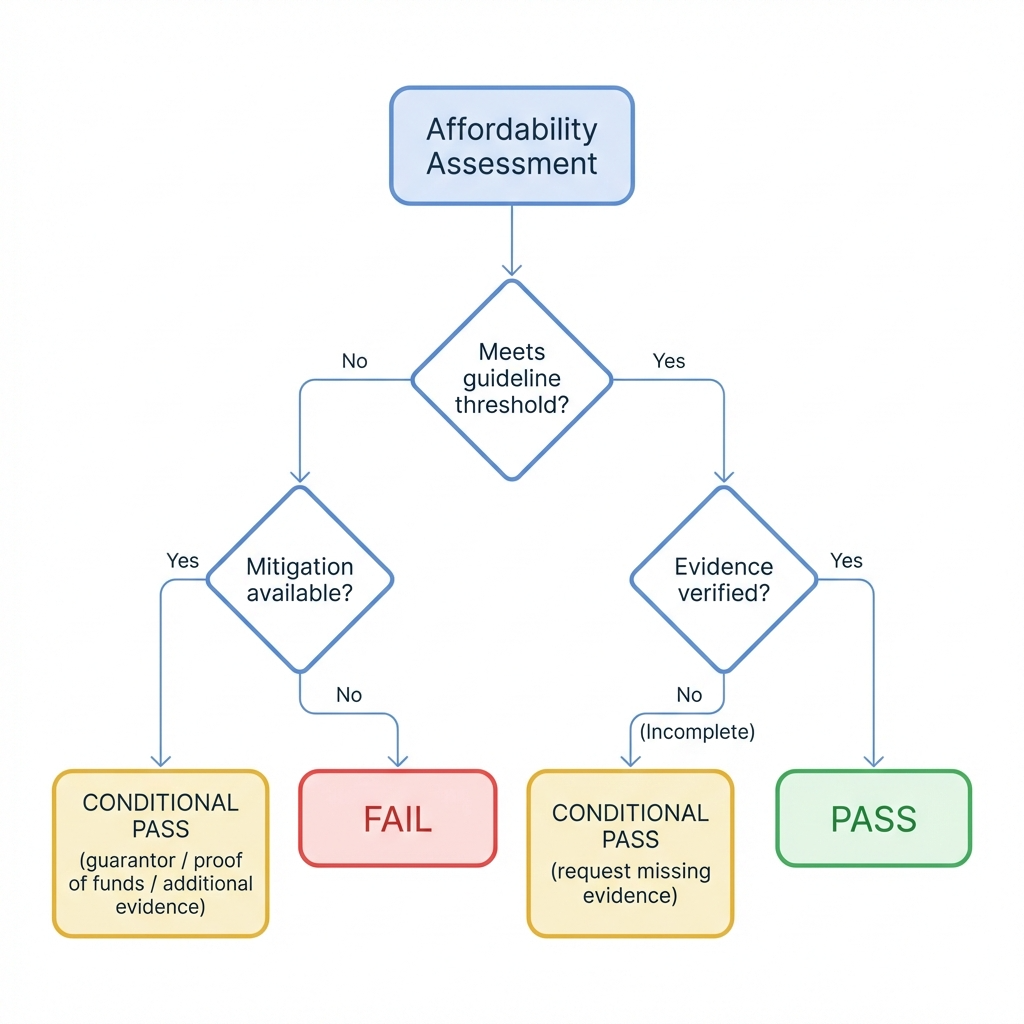

Decide outcome: Pass / Conditional pass / Fail

Define these outcomes upfront so decisions are consistent.

- Meets guideline thresholds

- Income verified

- No major red flags in stability or commitments

- Guarantor

- More evidence

- Higher deposit (where lawful)

- Document condition + deadline

- Clear shortfall, no mitigation

- Evidence inconsistent

- No confirmed income before move-in

Guarantors: when to require one — and how to do it properly

Guarantors shouldn't be a last-minute scramble. Build them into your policy.

Require a guarantor when:

- Affordability is below threshold

- Tenant has limited income history (student / new role)

- Variable or overseas income introduces timing risk

Guarantor checks should mirror affordability logic:

- Verify guarantor income and stability

- Confirm they understand the liability

- Ensure documentation is complete and consistent

The affordability checklist — copy/paste for your team

Pre-qual (5 minutes)

- Rent amount and move-in date confirmed

- Employment type confirmed

- Estimated monthly net income confirmed

- Any other household incomes confirmed

- Guarantor available if needed

Evidence pack — by tenant type

- PAYE: 3 payslips + bank statements showing salary credits

- Self-employed: SA302/tax calc + bank statements + accountant letter (if available)

- Contractor: contract + bank statements + renewal evidence if possible

- Overseas: contract/offer + proof of funds + bank statements

Decision record

- Applied threshold(s)

- Outcome: pass / conditional pass / fail

- Conditions (if any) + deadline

- Manager sign-off for edge cases

Common mistakes that slow your team down

- Improvising evidence requests → standardise a checklist by tenant type

- Starting referencing too early → run pre-qual first, then verify

- Inconsistent decisions → written thresholds + manager sign-off rules

- Over-collecting data → keep requests proportionate and policy-driven

- No decision record → document outcome rationale every time